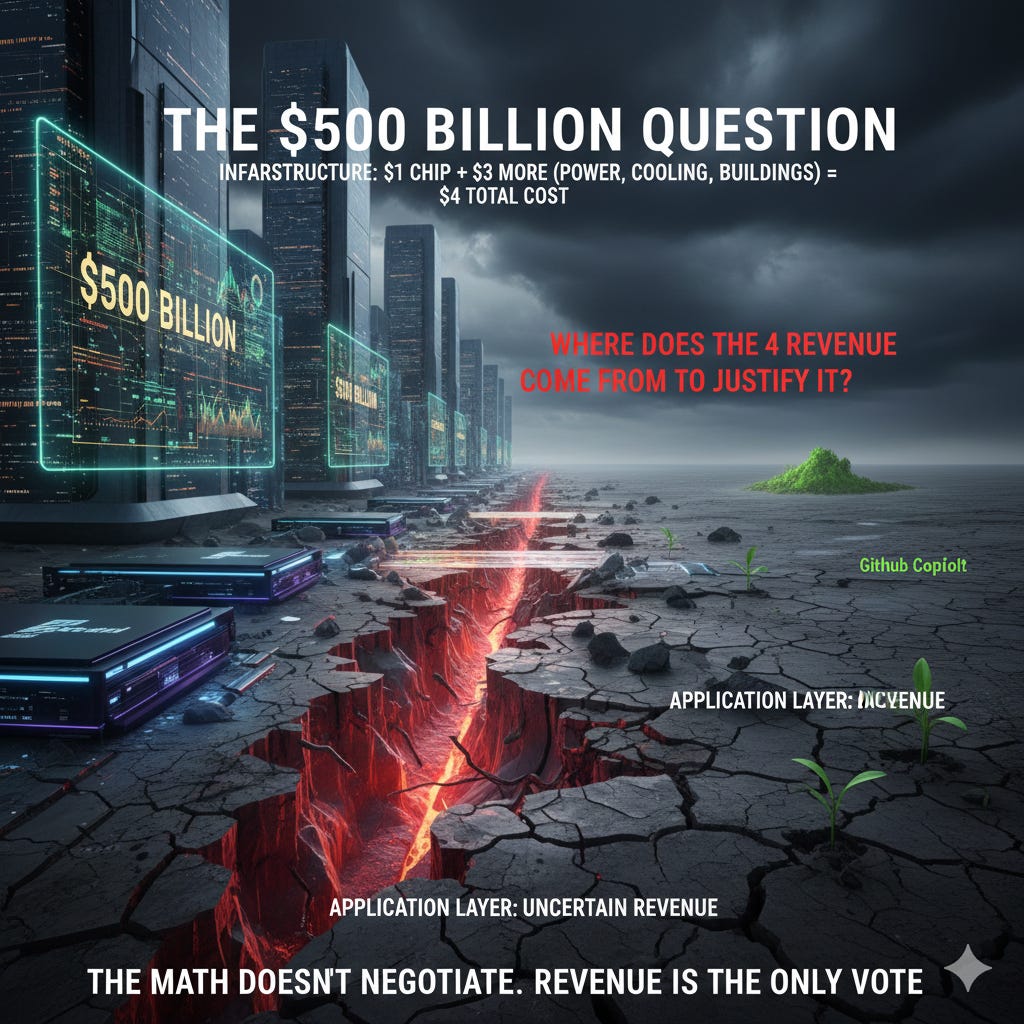

The $500 Billion Question

When Infrastructure Outruns Revenue

In early 2026, one number began circulating quietly through the AI industry:

$500 billion.

That is roughly the scale of AI hardware demand projected around Nvidia’s next‑generation chip cycles.

The figure refers primarily to the Blackwell and Rubin architectures — chips designed to power the next wave of large models, inference systems, and AI‑native applications.

The infrastructure is real. The spending is real. The demand signals are real.

But beneath the excitement sits a quieter question:

Where does the revenue come from to justify it.

The Arithmetic Beneath the Hype

AI infrastructure is not just chips.

For every dollar spent on a GPU, there are additional costs:

electricity

cooling

networking

buildings

maintenance

staffing

financing

A widely circulated heuristic suggests:

$1 on chips requires roughly $3 more to build and operate the full system.

Meaning:

$1 of hardware cost

$4 of total infrastructure cost

To make that investment rational, the system needs:

at least $4 in durable revenue for every $1 spent on chips.

This is not arbitrary. It reflects the economics required to:

cover infrastructure costs

generate operating margins

justify the equity valuations assigned to AI companies

If margins fall short, the entire stack reprices.

The Infrastructure–Revenue Cycle

Historically, infrastructure has often preceded revenue.

Railroads (19th century) Tracks were laid far ahead of demand. Many companies collapsed.

Electrification (early 20th century) Grids were built before industrial adoption caught up.

Fiber optics (late 1990s) Trillions were spent. Much of it went dark after the telecom crash.

Cloud computing (2000s–2010s) Years of losses preceded durable profitability.

The pattern is consistent:

Infrastructure built on future expectations

Revenue arrives more slowly than promised

Many participants fail

Survivors consolidate and eventually profit

The comforting story is:

Infrastructure comes first. Revenue follows.

The complete story is:

Infrastructure comes first. Most of it loses money. Then the industry consolidates.

The Belief Gap

Today’s AI infrastructure boom follows the same structure.

The hardware layer is generating enormous revenue:

Nvidia reporting record sales

Data centers expanding globally

Cloud providers racing to deploy capacity

But the application layer is less clear.

Startups are:

raising capital

building products

generating usage

Yet relatively few are producing large, durable, high‑margin revenue streams.

This creates a belief gap:

The infrastructure assumes massive future income.

The current software layer does not yet produce it.

As long as investors believe the revenue will arrive, the system holds.

If belief weakens, the adjustment is fast.

Because data centers cannot be unbuilt. And specialized chips are not easily resold.

The $4 Question

The key issue is not whether AI is useful.

It clearly is.

The real question is:

Can the application layer generate enough revenue to justify the infrastructure layer.

A simple framing:

For every $1 spent on chips, the world may need around $4 in sustainable AI‑driven revenue.

If that revenue appears, the system stabilizes. If it does not, the infrastructure reprices.

Who Captures the Value

Another structural question:

Where does the profit actually concentrate.

Right now:

Chipmakers are highly profitable.

Cloud providers are spending heavily.

Startups are burning capital.

Enterprises are experimenting.

If most of the value remains:

at the hardware layer,

while the application layer struggles to monetize,

the outcome is not:

“AI transforms everything.”

It is:

“AI enriches the infrastructure providers while most participants lose money.”

This is not unprecedented.

It is exactly what happened in:

railroads

telecom

early internet infrastructure

An Existence Proof: Copilot

There are early signs of durable AI revenue.

One of the clearest is:

GitHub Copilot.

It is:

a real product

with real customers

generating recurring revenue

delivering measurable productivity gains

It shows that AI can create:

direct value

at scale

with a viable business model

But the open question remains:

Are there enough Copilot‑like products to support $500 billion in hardware?

Or is that level of revenue still hypothetical?

The Circular Financing Risk

Another concern is the appearance of demand.

In some cases, hardware vendors:

invest in AI startups,

which then use that capital

to buy more hardware.

This creates a loop:

Capital flows from infrastructure providers into application companies and then back into infrastructure purchases.

On paper, this looks like demand. In reality, it can be vendor‑funded growth.

Not fraudulent — but structurally fragile.

The revenue appears in the hardware layer before it exists in the application layer.

The Monoculture Risk

The industry is not just building infrastructure.

It is converging on a single paradigm:

large models

centralized data centers

expensive GPUs

enormous energy consumption

This is not diversification.

It is monoculture.

Monocultures are efficient until something changes.

Then they become fragile.

How Belief Gaps Resolve

When infrastructure assumes revenue that has not yet materialized, there are only two outcomes.

1. The revenue arrives New industries form. Applications scale. The infrastructure bet is vindicated.

2. The revenue disappoints Margins compress. Investors pull back. The infrastructure reprices.

There is no third option.

Because:

the math doesn’t negotiate.

The Real Question

The $500 billion figure is not the problem.

Infrastructure waves always look excessive while they are being built.

The real question is simpler:

Is AI generating enough real economic value, fast enough, to justify the infrastructure being constructed?

That is not a philosophical question.

It is arithmetic with an uncertain numerator.

And eventually, revenue is the only vote that counts.